“Edosa, check out these guys…I just put ₦300k, but I want to put more…they give 25% in 3 months, let me know what you think…are they legit? Excerpts from a phone call with a friend of mine last weekend. I have grown accustomed to variations of this question mostly from millennials. So, I did some thinking.

The rate is so high, that it seems too good to be true. Why would someone want to take the risk? We have all heard stories of similar investments going bad – delayed repayment, partial repayment, no repayment at all. So why do some give it a second thought?

Let’s take a few steps back. Let’s walk in the minds of someone facing this dilemma. Before being faced with the choice of investing in x or y, you probably already had a passive desire to invest someday (either with your idle cash or borrowed cash).

We are in the digital age, the age of information overload, so you probably have different investment options flashing at you on social media, blog posts, and so on. You see a few that pick your interest, then whenever you have the funds, you invest. All good so far.

The Right Risks

Also, a rule of thumb says, the younger you are, the more your appetite for risk. Young people usually have less dependents, less obligations, generally less to lose, so might as well take some risks. But are we taking the “right” risks?

“If you don’t know where you want to go, then it doesn’t matter which path you take.” Why am I investing? What do I want to do with the returns from my investments? I think we need to ask ourselves these questions more. If you are investing ₦100 to buy a car a year from now that cost ₦125, your main concern is to make ₦25 on your initial investment during the year. If you were investing ₦100 to pay for your rent of ₦125 by the end of the year, you will have a similar concern.

Some of my colleagues believe that we mostly invest simply to have more than we did yesterday, and to keep up with expenses (inflation is the unseen robber of those who have saved – Margaret Thatcher).

If this is true, then it explains our search for the highest possible return, and our dismissal of the possibility of losing our savings if our investment in x or y turns sour. Perhaps it is a behavioral bias in response to how investment opportunities are presented. The upside (expected rate of return) are highlighted and overly emphasized, with little mention about the risk. So in a quest to grow our wealth, we may be taking detrimental (and in some cases, unnecessary) risks.

Be Deliberate

Now we need young people to take risks, but it is also important that they take the “right” risk, lest we raise a generation that are scared and shy away from investing.

Perhaps young people should embrace goal-based investing. Tying a specific, measurable goal to each investment. Like the car and school fees example above. Although the desired return of 25% are the same, the sort of investment options you will consider to meet your goal for buying a car, are different from those you will consider to meet your goal of paying your rent.

Put differently, if you end up losing your entire ₦100 investment meant for rent, the consequence is vastly different and more detrimental than if you lose the ₦100 investment intended for buying a car.

The importance of the goal, and the timeline really help you narrow down the sort of investments you want to make in order to meet that goal. It fundamentally forces you to consider the risk, because you are no longer investing for a vague idea, but a specific & measurable goal that is important to you.

Voila! Now we have a better approach to deciding which investment option to go with. A follow up challenge could be the difficulty in finding suitable investment options that meet your unique needs. We will discuss this one day.

Jeff Bezos is currently the richest person in the world. With a net worth of about $155 billion. That is impressive! For context, let’s review his journey.

Stellar academic records followed by an early career in fintech, and banking. He then worked at a new hedge fund, before leaving to start Amazon in 1994.

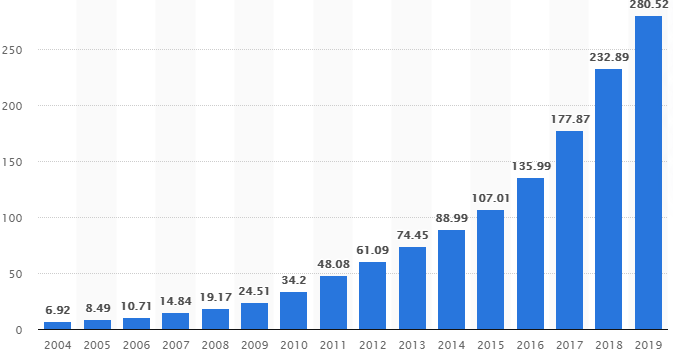

Amazon was a disruptor. The internet was still early back then, but internet users were increasing drastically. With this trend, Jeff Bezos was convinced that many of our activities could take place over the internet, including buying books. So, he started selling books online, going against established industry players such as Barnes & Noble who was still focused on brick and mortar stores.Today Amazon sells tens of millions of books annually. Also, they started offering more than just books. Today, Amazon is the marketplace for almost everything. They are prominent in electronics, grocery, and home appliances. They are also dominant in digital content (movie streaming), and cloud storage service (AWS). In 2019, the company generated about $280 billion in net revenue, and employees over 800,000 people worldwide. That is impressive!

Source: Statistica

With all this feat, Jeff Bezos can be said to be reaping the fruits of his labor. But how much is too much? Jeff owns about 11% of Amazon, which is where the majority of his wealth is attributed. As mentioned earlier, he is worth about $155 billion.

However, there has been lots of criticism about his net worth, or more broadly, criticism about a system that allows one person to amass so much wealth, while so many people are living in abject poverty, unable to afford necessities.

Some facts: indeed many people in the world are at risk due to poverty, indeed the wealth inequality (gap between the rich and the poor) seems to be getting bigger, and indeed Jeff Bezos, by any measure, is wealthy.

What worries me, however, is the fixation on a number. “Bezos is worth $155 billion, that is way more than he needs”, “it is unrealistic for regular people to catch up with him”. So let’s dig into this number.

Amazon, as a company, is valued at $1.3 trillion. Jeff Bezos owns 1% of the company, so his stake is worth ~$143 billion. He also owns a Space travel company, Blue Origin, and a media company, Washington Post, both of which are private so no public valuation information.

What is clear is that his stake in Amazon is the main contributor to his ~$155 billion net worth. Now, Amazon’s value changes every second based on the company’s share price, and by that measure, Jeff’s net worth changes every second. So Jeff Bezos is indeed wealthy, but as you can see, the bulk of his wealth is “locked up” and changes every second.

This is not to negate the extent of his wealth, but rather to shed some light on “Wealth available”. Meaning, what does he have at his disposal, that can be used to influence his standard of living? Jeff likely has a decent salary, and probably gets a healthy bonus in his compensation package, so by these measures, the wealth available to live well above average and splurge on luxury is very much in order. But this is still a fraction of his net worth.

When people think of Jeff Bezos net worth, and indeed, many other billionaires, the bulk of it, the tens of billions, are often “locked up” in an asset that changes price every second, and as such is more of “Wealth unavailable”. Now, not to be naïve, they can “unlock” this wealth by selling shares, borrowing against it, and using derivatives. But in many cases, their control/influence of the company, their attachment, and the tax implication, builds the incentive to keep most of this wealth “locked up”.

Imagine you had a painting in your house, passed down four generations, and now you. One day, your rich friend visits, and says she will buy the painting for $1 billion, the next day, an art collector says she will buy it for $3 billion. You put it up online, and you get similar offers.

At this point the consensus is that one of your possessions is worth about a billion dollars. Whether you sell it or not, you have an asset that is generally agreed upon by the market to be over a billion dollars, the market consensus could also change the very next day, giving your painting a different value.

With the painting and favorable consensus from willing and able buyers, now your net worth is +$1 billion. You see how that is vastly different from “wealth available” to you?

The following is a quarterly synopsis of what we have been up to and where we intend to go, with the aim of giving you an inside look into what we at Prairie Crossing are all about. Questions and comments are all welcomed, and can be directed to info@prairie-crossing.com.

LENDING

This past quarter we began our micro-lending service and we are proud to state that we have provided debt financing to two businesses in two very diverse but essential sectors of the Nigerian economy. One in the fashion industry, and the other in oil & gas industry.

Consistent with our focus on youth development, both firms are run by vibrant young entrepreneurs and their target market are mostly millennials, ages ranging from early 20’s to late 30’s. As we learn more and build capacity in the micro-lending service, we see ourselves providing loans to more small businesses in Q1 2019.

VENTURE CAPITAL

Aspire Digital Labs (@AspireLabs) remains our only equity investment to date. Established in January 2018, as a result of seed capital provided by Prairie Crossing. AspireLabs was created to boost the ICT learning experience for students in Primary and Secondary schools, thereby developing human capital through childhood education. The company currently manages the ICT program for two schools in Aba, Abia. Prairie crossing presently holds a 60% stake in the firm.

There seems to be growing awareness of the Prairie Crossing brand. This is partly due to our public relations and marketing efforts, and relevance of the financial services we offer. Our deal flow is growing steadily. We expect to make our second venture investment early next year and it will likely be within our area of focus: education, entertainment, consumer goods, and sports.

FINANCIAL MANAGEMENT SERVICE

Our main goal at Prairie Crossing is to help businesses perform better. From our foray in the venture capital world, and assessing founders, we realized that management skills are just as (if not more) important as access to capital. So we decided to start Prairie Financial Management Service (PFMS). With PFMS, we essentially take up the role of a CFO to small and mid-size businesses that do not have such expertise. It’s been fun so far, we dialogue with a lot more business owners these days and see economic activity from a different lens.

EVENTS

We had a huge honor of being part of “Lucid Lemons” annual event, this year’s third edition was called “Lemon Curd 3”. Lemon Curd is an event that showcases young talents in music, technology, art and food and promotes youth resilience.

At our section of the event, we hosted a GuysWhoCook competition, Wings Eating Contest, Advanced Virtual Reality Gaming and a Date Auction where the proceeds from this event, a total of fifty thousand naira, was donated to Food Clique, an organization that provides food for kids in disadvantaged schools.

Prairie crossing was also a part of the just concluded Atide ProjectBig Giveaway. ATIDE is a social enterprise that partners with select entrepreneurs and helps them increase not only sales but local and international awareness of their business and craft—in turn, a portion of sales goes towards a social cause.

This year ATIDE focused on renovating two low-income primary schools in Bariga, Lagos. Prairie Crossing was glad to be part of this event as donors, and volunteers. Between the 29th and 1st of October we along with other volunteers repainted both schools, cleaned the classrooms, set up a playground, and made gift packs for each student containing writing materials and books.

SUMMARY

The third quarter brought about the activation of 2 new arms – Lending, and PFMS. We have been working on them for a while, and are glad we were able to begin both this past quarter. Our first two charity events also took place in Q3. Investors sentiment on the economy seems to be bearish. Our reserves, which have played an important role in keeping our exchange rate stable, are on downward trend, currently at $43.9 billion from a high of 47.8 on the 7th of May 2018. The All Share Index is down 15.2% YTD. Rising crude oil prices and steady production remains a bright spot. We will continue to carefully craft and fine tune our new operations, so as to deliver exceptional services to both investors and clients.

To Stakeholders of Prairie Crossing Capital Management Ltd.

As we usher in another year, we like to reflect on the past twelve months. A sort of stock taking, before continuing the journey. The major question we at Prairie Crossing ask ourselves each year is, were we able to improve the quality of life for Nigerians?

On the macro level, nothing much has changed for the average Nigerian. The economy is growing at 1.81%, inflation rose by 11.44% YoY. Terrorist attacks persist in some parts of the Northeast, government workers continue to go on strike. In our own little way, we choose areas to work on that, when done right, would have a significant multiplier effect.

The first is to help businesses run better, and the second is to promote youth development. Investing in these two focus areas could change the quality of life for Nigerians – at least that’s what we think.

In 2018, we barely made a dent in the quality of life “index” of Nigerians. However, we believe that some of the services and products we started this year, have in them the right ingredients to scale and impact more lives. With that in mind, here are the highlights of 2018:

We kicked off our lending operations this year. The logic behind this was to provide micro financing for small businesses to help them meet specific needs.

Many small business, 3 to 5 years in, find it difficult to raise short term finance from traditional sources, despite their decent financial standing. The time between application and funding was mentioned as one of their pain points.

Starting from August 2018, we provided eight loan facilities to seven companies/projects. Our average loan amount was ₦500,000, and average tenure was 3.5 months. For loans we gave, average time from when we received application to when we funded was 5 days.

In 2019 we plan to standardize our review process, and be more hands on in assisting borrowers in management of loaned funds.

Our portfolio company Aspire Digital Labs Limited closed the year with revenue of ₦1.2 million, crossing the million naira mark. The firm missed some of our 2018 targets, mostly due to growing receivables (a pain in the neck for many small businesses), fortunately we’ve been working on some measures to curb unnecessary bottlenecks in payment collections, and subsequently turn the company profitable in 2019.

We launched our Financial Management Services, which includes: virtual CFO services to small businesses, valuation, and M&A advisory. Entrepreneurship can be a lonely and tasking journey.

Founders find themselves changing between a hand-held microscope, and telescope every other second. That is, having to be attune with the smallest details of their company one moment, and the next, detaching, to ponder on innovative disruption, and the future of their sector.

We hope that our financial management services provides the necessary complimentary skills to the C-Suite of small businesses.

We supported three great community programs this year with volunteer hours and/or financial donations.

The first was ATIDE, a social enterprise, we supported in their renovation of two low-income primary schools in Bariga, Lagos.

The second, Food Clique, an NGO set out to eradicate child hunger, held a community kitchen in November which we volunteered at. They were also recipients of our GuysWhoCook charity fund raiser.

The third, was a donation (we paid for 3 tickets to their fund raising comedy night) to the Joyful Joy Foundation, a non-governmental organization focused on combating malaria in Nigeria.

This year, in future, will be used as a case study as to how Nigeria managed a couple economic curve balls. Exchange rate volatility, growing fiscal deficit, and inflation.

Of course, these problems have been centre stage since mid-2014, when oil prices began its downward spiral. What was unique about this year, however, is the perception of progress.

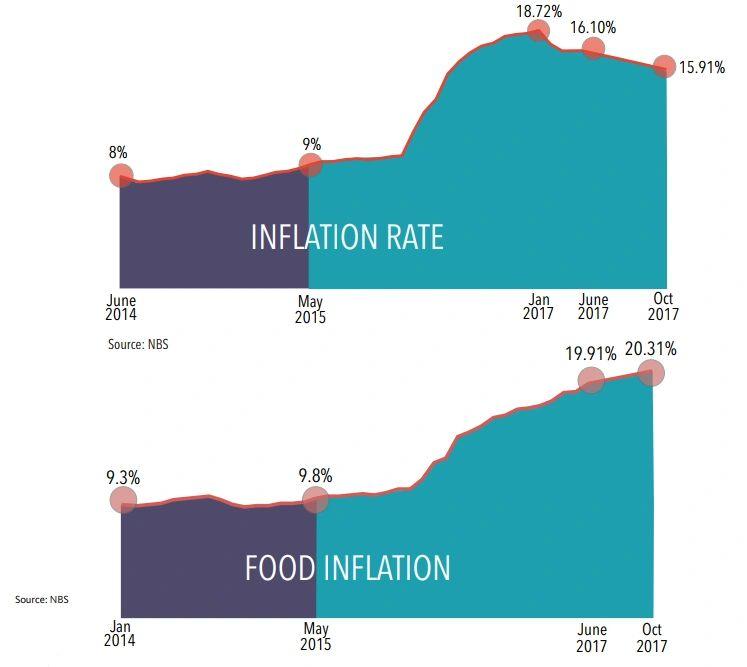

We witnessed economic indicators stabilize, and in some cases, get better. Naira has been relatively stable in the last half of the year, within a range bound of ₦359/USD to ₦367/USD from June to date. YTD, the NGN/USD has appreciated by about 35% in the parallel market. Both oil revenue, and non-oil revenue (mainly company income tax), continue to fall short of budgeted projections. Inflation painfully increased in 2016, and although curbing back in 2017 (currently at 15.9%), it remains substantially higher than the sub 10% rates of 2013-2015.

At the beginning of 2017, the market had lost appetite for equities due to crashing prices, and credit was the new favourite. However, at year end NSE All Shares Index is up 42% while S&P Nigeria Bond index closed the year up 26%.

As investors, these indicators mean a lot to us because as the economy grows the prospects of our ventures become even brighter. While Q1’s real GDP growth was negative, Q2 and Q3 recorded positive GDP growth of 0.72% and 1.40% respectively. GDP growth in the first nine months of 2017 comes out to 0.43%, according to the Nigerian Bureau of Statistics.

Our growth rate in the past year has been far from glamorous, but the trend is encouraging. To put in context, Q2 2017 recorded the first positive quarterly real GDP growth since Q4 2015. While the data points signal the likelihood of economic recovery ahead, the broader economy still faces many challenges.

To solve these challenges, the country will need a decisive and consistent monetary and fiscal policy going into 2018.

Prescription for economic growth

In the traditional sense, the economy grows when output is increasing. Fundamentally, output is made up of the following components – consumer spending, business investment, government spending, and net exports. For the economy to grow, incentives will need to be put in place to increase outputs.

Our first prescription is interest rate cuts. Monetary policy rate (MPR) in Nigeria stands at 14%, up from its 12% level in July of 2016. This will increase much needed liquidity in our economy, by lowering cost of capital. Resulting in increased private sector credit, and incentives for more investors to look for higher returns in the real economy.

Our second prescription is increased government spending. For an effective economic recovery in 2018, Nigeria needs increased government spending on capital projects in key sectors. Government spending on capital projects will help increase liquidity, and create jobs.

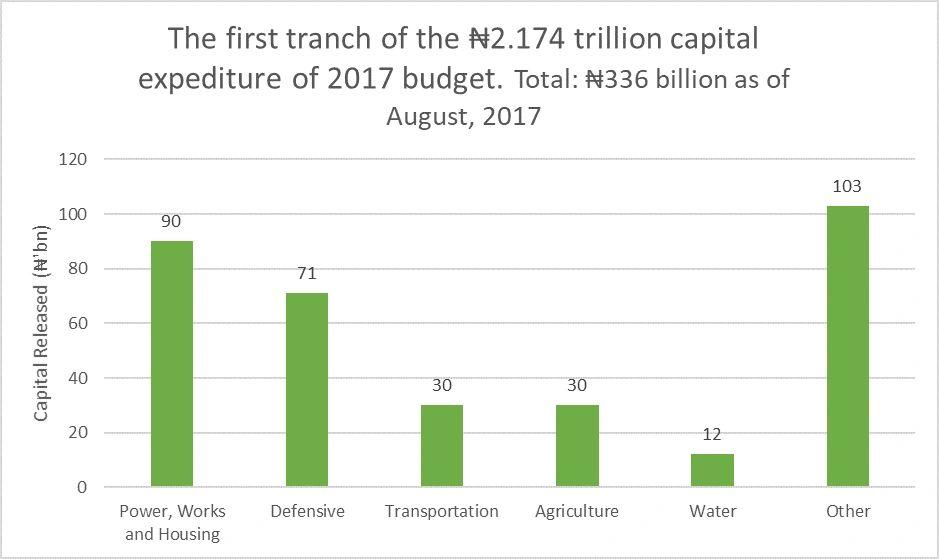

From our ₦7.4 trillion 2017 budget, government spending on recurring non-debt expenses (35%) and debt servicing (22%) were at cautionary levels, and rivals the 29% allocated for capital expenditure.

Capital expenditure in the proposed 2018 budget is ₦2.43 trillion, only up by 11% from last year’s approved budget. Comparatively, in the 2018 proposed budget, allocation for debt servicing increased by 20% to ₦2.01 trillion, and recurring non-debt expenses increased by 32% to ₦3.49 trillion.

The outcomes of these approaches

If our recommendations are taken, our Nation’s economic policy will essentially shift from contractionary to expansionary in 2018. With a combination of lower interest rate and increased government spending, one likely outcome is higher inflation.

Also, if these measures are taken, the Naira (₦), may weaken, which discourages importing. Another expected outcome from lower interest rate is the negative effect it will have on bank profits, and lenders in general, due to decreasing net interest margins.

While higher inflation, and weaker currency will hurt consumers, banks and businesses in the short run, economic growth will start to pick up in the medium term, putting individuals in a better situation.

Why these recommendations may not be taken

Retrieved from BudgetIT

Inflation is currently high in Nigeria; tapering interest rates will add upward pressure on inflation which becomes very burdensome for consumers.

With election cycle coming in, policies that will cost short term hardship to the masses in exchange for future economic growth, may not be the preferred choice for the incumbent.

Secondly, as the 2018 proposed budget shows us, the government does not have the capacity to put sizeable funds to work on capital expenditure.

So, what can we expect in 2018?

This year, government spending on capital expenditure will increase from previous year’s level. The 2018 proposed budget supports this as well.

However, a paltry 11% increase is far from what the economy needs. Government revenue is bound to increase in 2018, as average oil prices are likely to be higher than 2017’s average.

Oil will remain the main driver of increased revenue. Oil prices have recovered well over a third of their value since hitting 2017 lows in June. We expect that average oil price in 2018 will be moderately higher than it was in 2017, in part due to the OPEC-led commitment to extend production cuts, and stronger demand.

With relatively moderate increase in government spending, and only modest decrease in interest rate, we expect increased liquidity in the market, albeit far from what the economy needs for a health economic recovery.

We believe that Central Bank of Nigeria (CBN) and government will forego the aggressive economic stimulus as recommended earlier, and continue with either contraction or the half-baked stimulus described in the above paragraph.

Hence, we can expect to see relatively stable inflation levels, and a less volatile exchange rate. Although we don’t think this is the best approach for economic growth, it does have some short to midterm advantages. For one, this sort of stability will increase both investor and consumer confidence.

All about the Naira

The Naira appreciated in 2017, mostly due to rise in oil price, and interventions by CBN – increase in interest rates. We believe that both factors will be at play in 2018 as well. Oil importers, investors, exporters, and pilgrims had exchange rate windows that offered more favourable rates in 2017. This succeeded in attracting foreign investors.

As an economy grows stronger, foreign investments will be channelled into the economy, which increases demand for local currency. While the Nigerian economy is expected to be relatively stronger in 2018, foreign investors have other options to deploy funds to, there are other economies with not as much risk, or similar risk that have healthier growth. So, we can’t expect the Naira to strengthen on the back of a greater projected economic growth in 2018.

With high interest rates, we can expect continuous flow of foreign portfolio investments, provided the I&E (NAFEX) window is maintained, which will be good for the Naira.

We believe that Naira, while still overvalued, will be more stable in 2018, with modest appreciation, mostly due to CBN intervention. The biggest risk however to the Naira remains oil price.

Summary

Given these, our GDP growth in 2018 will be greater than that of 2017, but far from eye-watering. Hence, it is no surprise that IMF forecasts 2.1% GDP growth for Nigeria in 2018, which is far below the global forecast of 4% by Goldman Sachs.

In the stock market, the task will be to discern stocks beaten down by systematic risk alone from those that are beaten down by both systematic risk and fundamentals. Investors will need to be more vigilant, and industry-specific in the coming year.

Important Disclosure: None of the market information, data, and company information presented herein constitutes a recommendation by Prairie Crossing Capital Management, or a solicitation of any offer to buy or sell any securities. Readers should note that information presented is general information that does not take into account your individual or institutional circumstances, financial situation, or needs, nor does it present a personalized recommendation to you.